Proposition 1 funding

Funding needs and potential sources

On Nov. 4, 2014, 80 percent of Texas voters approved the ballot measure known as Proposition 1, which authorized a constitutional amendment for transportation funding. Under the amendment, a portion of existing oil and natural gas production taxes, also known as severance taxes, would be divided evenly between the Economic Stabilization Fund and the State Highway Fund. Pursuant to Section 49-g(c), Article III, Texas Constitution, the funds may only be used for constructing, maintaining, and acquiring rights-of-way for public roadways other than toll roads.

Ballot proposition language:

The constitutional amendment providing for the use and dedication of certain money transferred to the state highway fund to assist in the completion of transportation construction, maintenance and rehabilitation projects, not to include toll roads.

Background

The 83rd Legislature (Third Called Session, 2013) passed Senate Joint Resolution 1, which amended the constitution to include Proposition 1 funding, and House Bill 1, which created a sufficient balance committee to determine a minimum balance of the ESF before transfers of severance taxes to the SHF may begin to occur. The minimum level of ESF funding is known as the sufficient balance.

The 86th Legislature (Regular Session, 2019) passed Senate Bill 69, which automated the process of selecting the sufficient balance threshold. The balance threshold is now determined to be at a level equivalent to seven percent of the amount of certified, general revenue-related appropriations for that fiscal biennium, as determined by the Texas Comptroller of Public Accounts.

The 88th Legislature (Regular Session, 2023) passed House Bill 2230, which extended the expiration of Proposition 1 fund transfers to the SHF to December 31, 2042.

Methodology

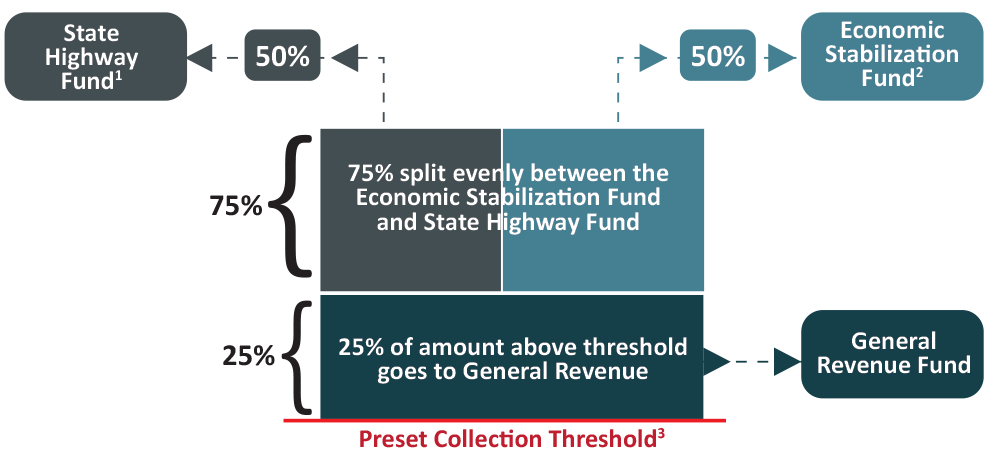

Figure 1 explains the method of transferring severance taxes to the SHF. It begins with a preset collection threshold consisting of fiscal year 1987 oil and natural gas production tax levels. Oil production tax revenues in FY 1987 were $531.9 million and natural gas production tax revenues in the same year were $599.8 million. A quarter of total severance tax collections above the threshold are deposited into the state’s general revenue fund. The remaining severance taxes are divided evenly between the ESF and SHF. However, before transfers to the SHF may occur, the balance of the ESF must be at least seven percent of the amount of certified, general-revenue-related appropriations for the fiscal biennium as determined by the comptroller.

Proposition 1 deposits to the SHF

Proposition 1 deposits to the SHF fluctuate from year to year because they depend on annual oil and natural gas production. The table below shows Proposition 1 transfers to the SHF from FYs 2015-2021.

| Fiscal year | Deposits to SHF | Total deposits to date |

|---|---|---|

| 2015 | $1.74 billion | |

| 2016 | $1.13 billion | |

| 2017 | $440 million | |

| 2018 | $734 million | |

| 2019 | $1.38 billion | |

| 2020 | $1.67 billion | |

| 2021 |

$1.13 billion |

|

| 2022 | $1.46 billion | |

| 2023 | $3.64 billion | |

| 2024 | $3.06 billion | |

| 2025 | $2.74 billion | $19.1 billion |

Factors affecting Proposition 1 deposits to the SHF

Some of the factors affecting Proposition 1 deposits are as follows:

- Fluctuations in oil and natural gas production may affect Proposition 1 deposit amounts.

- Currently, the sufficient balance of the ESF is seven percent of the certified general revenue-related appropriations made for the fiscal biennium, as determined by the comptroller. A higher sufficient balance or legislative appropriations made from the ESF that reduce the amount of cash available to meet the sufficient balance could mean less money is available for transfer to the SHF.

- Proposition 1 funds are set to expire after the FY 2043 (November 2042) transfer if the legislature does not extend the statutory expiration date.

More information

For media inquiries, email Media Relations or call 512-463-8700. For inquiries from the public, legislative offices or other government offices, contact State Legislative Affairs.